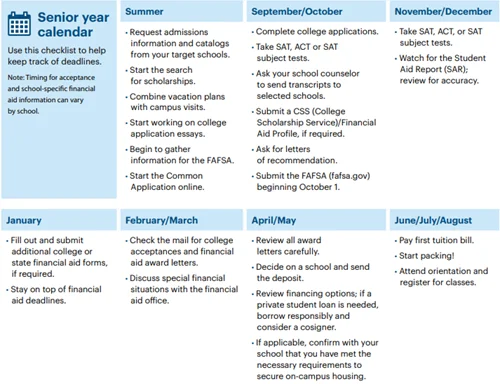

Paying For College Responsibly

Use the 1-2-3 approach to help your student pay for college

When you’re planning for college, the first question is often which school to choose. But equally as important is the question of how you’ll pay for it. That’s why we’ve partnered with Sallie Mae® to bring you their 1‑2‑3 approach to paying for college. These three steps can help you make more informed, responsible financial decisions for a big investment in your future.

1. Start with money you won’t have to pay back. Supplement your college savings and income by maximizing scholarships, grants, and work‑study.

Begin with any college savings that have been put aside in a dedicated college savings account and include current income that you’re earmarking for college. Maximize “free” money you will not have to pay back, including scholarships and grants. Then consider work‑study.

Scholarships

Scholarships are offered by colleges and universities, federal and state governments, religious groups, professional associations, employers, and other companies. You might think they’re only for academic or athletic accomplishments, but they can be awarded for a number of criteria:

- Organization memberships

- Community leadership

- Financial need

- Ethnic, religious, or national background

Apply for scholarships—the earlier, the better, since many have deadlines.

Grants and work‑study

Grants and work‑study are generally federally funded, so be sure to submit the Free Application for Federal Student Aid (FAFSA) to apply for them. The FAFSA is also used to apply for most state loan, grant, and scholarship programs.

- Pell Grants, the largest federal grant program, are based on financial need; unlike a loan, a Pell Grant doesn’t need to be paid back.¹

- Work‑study programs are offered by federal and state governments, as well as schools. They offer part‑time jobs that let students earn money to help pay education expenses.

2. Explore federal student loans. Apply by completing the Free Application for Federal Student Aid.

After you’ve maximized your free money, consider federal student loans, which are provided by the government. Direct Subsidized Loans are for students with demonstrated need and Direct Unsubsidized Loans are available regardless of family income.

- You can apply for both by filling out and submitting the FAFSA.

- They’re issued in the student’s name and the student is responsible for paying them back.

- They’re eligible for income‑driven repayment plans that link monthly payments to income.

- Federal loans may be eligible for loan forgiveness programs, such as the Public Service Loan Forgiveness Program for borrowers who are employed by a qualifying public service organization.

3. Consider a responsible private student loan. Fill the gap between your available resources and the cost of college.

If you still need additional funds after following steps 1 and 2, consider a private student loan. Private loans differ from federal student loans in several ways:

- They’re originated by banks and credit unions.

- They’re credit‑based: the lender reviews your credit score and history to determine if you qualify. A cosigner— parent, guardian, or other adult—may improve the chances of approval. Some lenders offer a cosigner release option.

- Your interest rate is based on several factors, including your creditworthiness.

- Private student loans may offer different features, terms and options, and benefits that can help reduce your interest rate and/or total loan cost.

Borrow responsibly

We encourage students and families to start with savings, grants, scholarships, and federal student loans to pay for college. Students and families should evaluate all anticipated monthly loan payments, and how much the student expects to earn in the future, before considering a private student loan.

1 See https://studentaid.gov/understand-aid/types#grants for more information. Sallie Mae does not provide, and these materials are not meant to convey financial, tax, or legal advice. Consult your own attorney or tax advisor about your specific circumstances. Grant, work‑study, and federal student loan information was gathered on June 23, 2021 from Studentaid.ed.gov. Sallie Mae, the Sallie Mae logo, and other Sallie Mae names and logos are service marks or registered service marks of Sallie Mae Bank. All other names and logos used are the trademarks or service marks of their respective owners. SLM Corporation and its subsidiaries, including Sallie Mae Bank, are not sponsored by or agencies of the United States of America. © 2021 Sallie Mae Bank. All rights reserved. SMPC MKT16050A 0621